What’s the outlook for enterprise hard disk drives (HDD) in the data center?

Will the current surge in demand for affordable high-cap storage keep HDD on top? Or are solid state drives (SSD), fueled by long-term declines in NAND flash prices, on track to eclipse enterprise HDD as the dominant storage technology?

After years of supply chain turbulence which rattled the tech industry, demand for HDD is back in force. While recent HDD shortages have led some to suggest QLC NAND is the future of mass storage, enterprise HDD will likely maintain a central role storing data cheaply at scale for the foreseeable future. After all, most data still resides on spinning platters, and the dawn of mass-market HAMR drives is allowing OEMs to ramp up areal density.

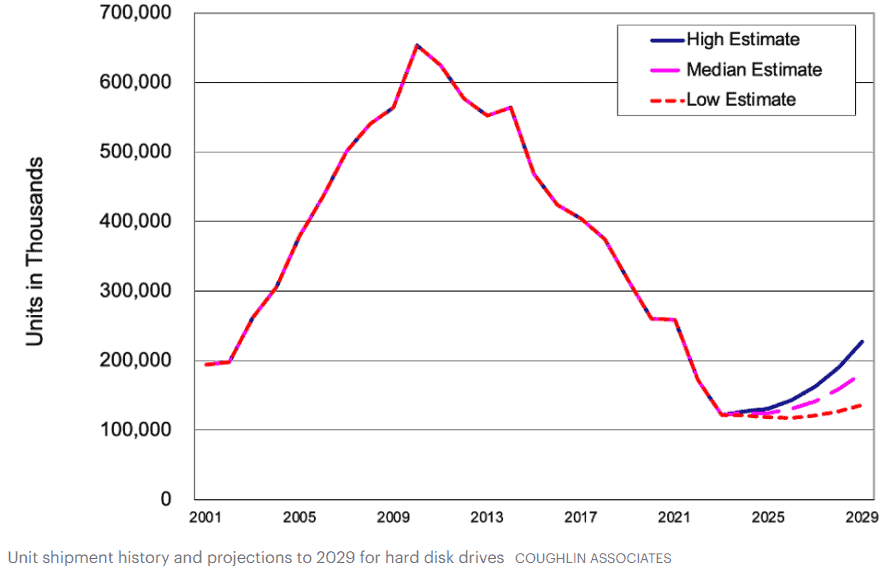

Good Times for Hard Drives

For a contrast to the current storage landscape, let’s look back a few years. These were trying times for HDD manufacturers.

In 2Q2022, there was a 33% y-o-y sharp drop in shipped units due to reduced demand for consumer HDD. A year later, it was clear the decline was also coming for nearline drives, with 3.5” high cap drives seeing a stunning 45% drop in shipped units in 2Q2023. But flash was hurting too. In early 2023, Micron saw its worst downturn in 13 years, Samsung’s profits hit an 8-year low, and Intel posted the largest loss in its history.

However, demand soon picked up again. According to analyst Tom Coughlin, 2024 saw an estimated 42% y-o-y increase in unit volume shipments of high-cap nearline hard drives. Overall HDD capacity shipments also increased by an estimated 39% y-o-y, and HDD revenues by an estimated 49% y-o-y. The message was clear: HDD had returned.

Today, Seagate and Western Digital are using the high demand to their respective advantages. In 1FQ2026, revenue was up 21% for Seagate and up 27% for WD.

The Relentless Rise of Data Storage

It’s no secret what’s driving all of this demand. The AI craze is leading to rising storage spend, as companies race for the space they need to store training data and AI output.

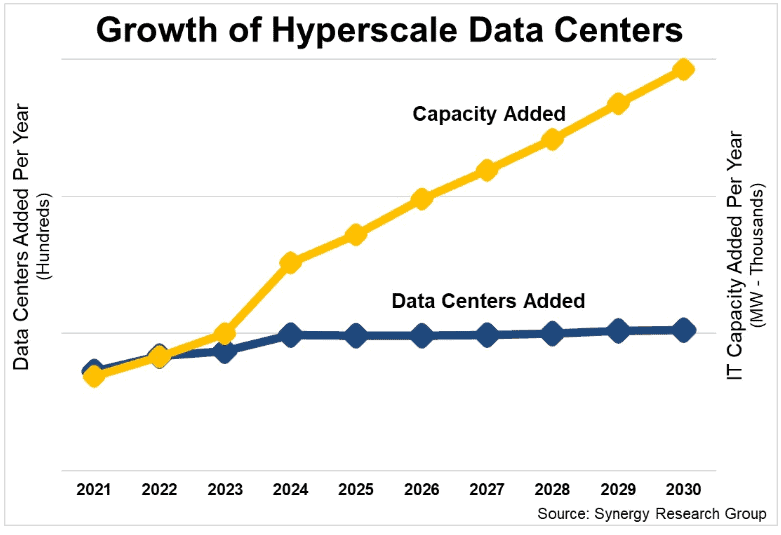

Growth in data center construction

According to Synergy Research Group, hyperscalers were operating 1189 data centers by the end of 1Q2025. Together, these centers held 44% of worldwide data center capacity. Synergy’s big prediction: total hyperscale data center capacity will almost triple by 2030.

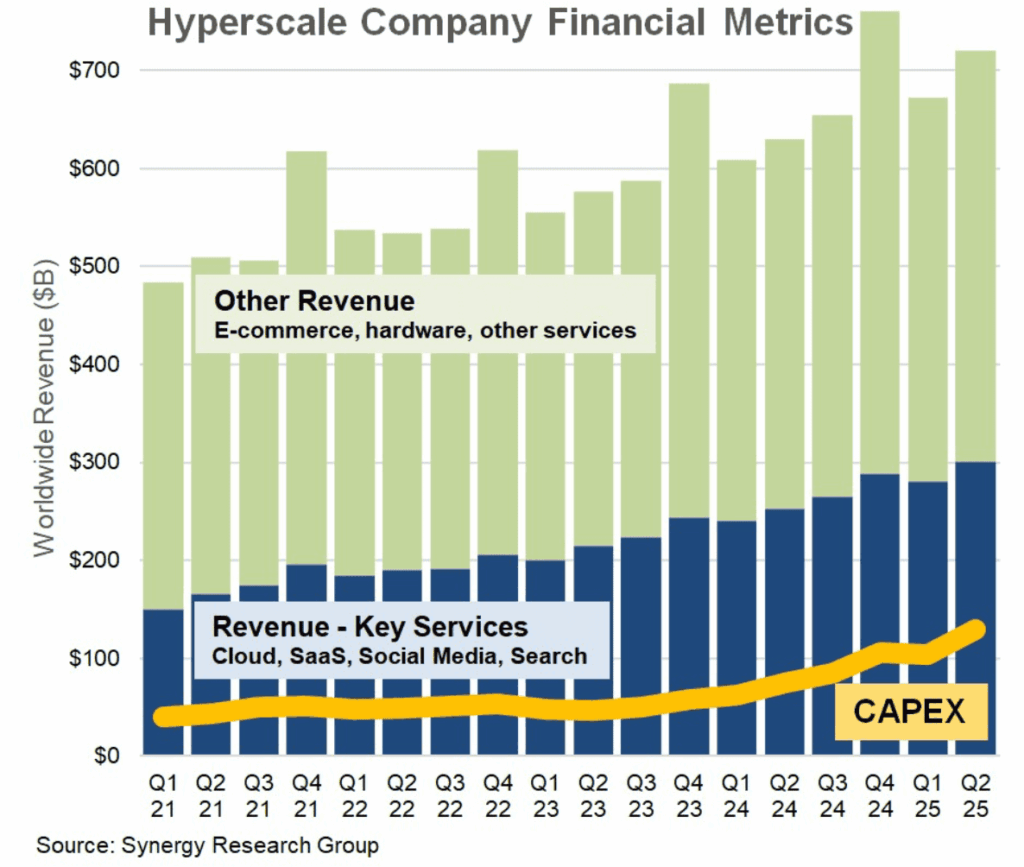

Growth in Revenue & CapEx

A tripling of capacity between now and 2030 may seem like a big jump. However, Synergy believes hyperscalers have the revenue to make it happen. For the past 8 quarters, operating revenue in key digital services (including infrastructure-, platform-, and software-as-a-service) has grown 18% y-o-y. CapEx has grown to match, and has been up 72% y-o-y in each of the last four quarters.

That spending means a lot of exabytes, the lion’s share of which will be on spinning platters.

Growth in cloud storage

Speaking of hyperscalers, cloud storage growth as measured by spend is still going strong. According to Synergy’s most recent report on cloud spend, in 3Q2025, expenditure jumped by $7.5 billion q-o-q. This marked the biggest sequential increase ever. Quarterly cloud infrastructure service revenues were $106.9 billion.

According to IDC estimates, 89% of data stored by lead cloud service providers still resides on HDD. If that continues, HDD is about to have a big few years.

Of course, it’s not an either-or situation when it comes to storage technologies. Tape serves as a good analogy here. It remains unlikely that HDD will develop into a credible threat to tape as a medium for cold storage in the hyperscale data center. Just as tape still has its place in the storage mix, enterprise HDD will likely retain its place in the cloud as the data storage workhorse.

Related Reading

Even as its use declined elsewhere, magnetic tape has carved out a niche in archival storage.

Get That On Tape: The Past and Future of Magnetic Tape Storage

HDD and SSD

When it comes to demand, can there be too much of a good thing? Trendforce has found that hyperscalers’ appetite for HDD is resulting in a severe shortage of nearline drives, leading some to turn to QLC NAND as a stopgap in the meantime. This has led to a rise in prices: according to Coughlin, in 2Q2025 hard drive ASP was the highest it had been since 1998. Worries were further stoked by the recent omission in WD and Seagate’s recent earnings reports of data on number of units shipped. Leaving this out makes determining ASP far more difficult.

What’s more, flash is already the default choice for storage outside of the data center. “HDD makers have long since recognized the inevitability of the notebook entirely transitioning to SSD,” remarks Stephen Buckler, chief operating officer at Horizon Technology.

However, this does not spell the end of the hard drive, Buckler insists. “Increasingly storage is all about the cloud. As AI and big data play an ever greater role in our day-to-day lives, this increases the need for cheap storage. Storage leaders such as Seagate and Western Digital continue to invest in improvements to hard disk technology, signaling that the game is far from up for HDD.”

AI is a major driver of demand for storage. According to a Recon Analytics survey commissioned by Seagate, 61% of correspondents said their cloud-based storage would more than double over the next three years. And when it comes to data retention, 90% believed the practice improved the quality of AI outcomes.

There are a few additional points to keep in mind. Firstly, the pricing situation isn’t just an HDD problem. According to DigiTimes, NAND and DRAM prices for 4Q2025 are up by an estimated 15-20% sequentially. Samsung’s V9 NAND is nearly sold out for 2026, and in September, SanDisk pushed for a 10% NAND hike.

Limits to manufacturing will also help keep HDD in play. Pure Storage R&D VP Shawn Rosemarin argued in 2023 that there would be no more HDD sales after 2028. But Chris Mellor at Blocks & Files estimates that even given advances in flash capacity, NAND production in 2029 will fall about 405EB short of what would be needed to replace HDD capacity. These limitations on the pace of SSD fab construction ensures that HDD will remain critical in the years ahead.

Related Reading

Long a hot-button topic, TCO comparisons between all-flash and HDD solutions have gained new importance in the face of changing data centers. But a simple truth still holds: it all depends on the use case.

Sunny Forecast for HDD

Unsurprisingly, this huge boost in hyperscale data center capacity and cloud spending will likely lead to a continued rise in shipped capacity for nearline HDD.

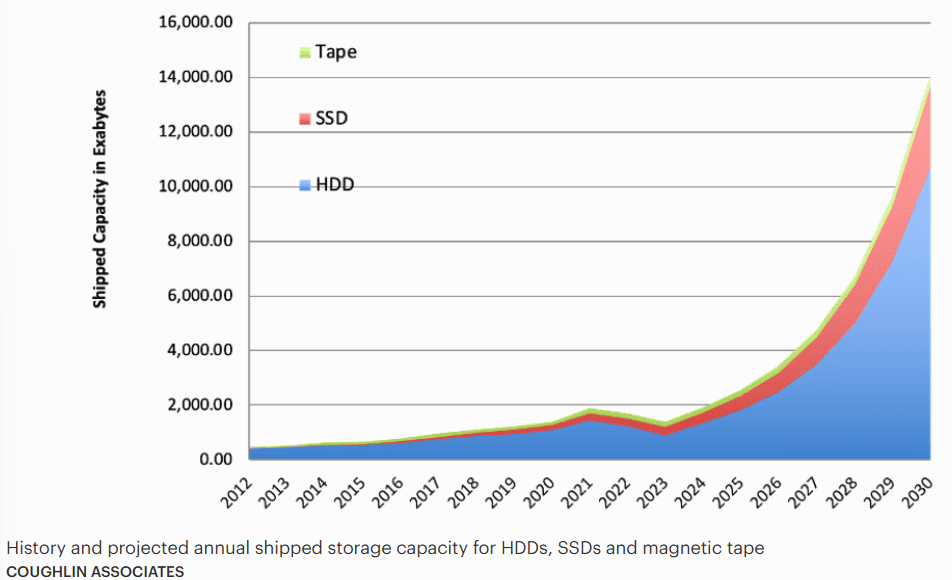

Tom Coughlin believes that HDD capacity shipments will be around 7.3ZB by 2029. He further predicts that nearline HDD will comprise over 90% of these shipments, compared to 54% today. HDD won’t be the only beneficiary of the boom: Coughlin projects that HDD, SSD, magnetic tape, and optical should all see their capacity shipments grow 5x between 2024 and 2029.

As for QLC NAND, Coughlin believes that high-cap SSD will also drive HDD demand. He predicts that AI focused companies will use flash data lakes to feed memory attached to GPUs, with cheaper spinning media remaining the go-to for long-term storage. As for current HDD shortages, Coughlin argues that they are temporary, and that HDD will be able to meet the high demand for capacity.

Related Reading

Each of the big three hard drive OEMs have set out ambitious roadmaps to take them to 50TB and beyond.

New HDD Technologies

There remain good grounds for the three main hard drive makers to feel very optimistic about the medium-to-long-term outlook for HDD.

HDD manufacturers have been squeezing in extra platters, and dabbling in multi-actuator technology, which is designed to unlock additional IOPS for improved read/write performance. And increasingly, OEMs are upping the ante on areal density with the use of heat-assisted magnetic recording (HAMR).

True to its name, Seagate’s Exos M 32TB HAMR drive packs 32TB into only 10 platters. From there, the firm plans to move to 36TB, 40TB, and 50TB drives, each with greater areal density than the last. The firm has already experimented with 5TB disks in the lab. While no firm dates were given, Seagate CFO Gianluca Romano expects that there will be a gap of 18-20 months between HAMR capacity increases.

Related Reading

Giving areal density a much-needed boost, heat-assisted magnetic recording (HAMR) is crucial to manufacturer capacity roadmaps.

Western Digital is also taking the HAMR route, with 36-44TB drives expected by 2026. Some of its HAMR drives will still use SMR technology (shingled magnetic recording) for an additional capacity boost. With SMR and 11 platters per drive, WD is prioritizing reduced qualification periods over Seagate’s no-frills 10-platter HAMR design.

While the technical approaches may vary, what appears certain is that HDD is poised for significant capacity growth in the years ahead.

Catch a Rising Tide

The future storage mix is always tricky to predict, as unexpected innovations can lead to rapid change. But for the moment, with strong demand for spinning media and HAMR delivering long-promised increases in areal density, HDD is likely set for a boom over the next few years. Hard drives currently dominate as a share of data center storage, and this is unlikely to end anytime soon.

At the same time, flash continues to strengthen across storage use cases. It will continue to grow as a proportion of an expanding pie. In a world of diverse storage uses, analysts would do well not to overemphasize the conflict between HDD and SSD. After all, the surge in data generated means there will be a massive amount to store and process. This suggests an all-hands-on-deck scenario where multiple varieties of storage work in tandem. A rising tide lifts all boats, as they say.

Whether you’re buying or disposing of data storage capacity, learn more about how Horizon Technology leverages its deep industry expertise to support your enterprise hard drive needs.